Blockchain technology, once known primarily as the backbone of cryptocurrencies, has evolved into a transformative force across various industries. This comprehensive guide explores the diverse ways blockchain is revolutionising industries worldwide.

Understanding the blockchain’s key technology is crucial as it forms the foundation of ensuring data security and allowing for decentralised consensus. Table 1 explains the key terminologies of the blockchain that need to be understood by the user.

Table 1: Key terminologies commonly used in blockchain technology

| Name | Description |

| Block | A data structure containing a batch of verified transactions. |

| Hash | A unique alphanumeric string that is derived using a mathematical function to identify blocks and their contents securely. |

| Consensus algorithm | A protocol used in blockchain networks to achieve the necessary agreement. A consensus algorithm that requires a participator to solve a numerical problem is complex to solve but easy to verify. |

| Proof of Work (PoW) | PoW is used in cryptocurrencies, such as Bitcoin, to validate transactions and mine new blocks. |

| Proof of Stake (PoS) | A consensus mechanism used in blockchain networks to achieve an agreement on the state of the ledger. |

| Smart contract | A self-executing digital contract encoded with predefined rules and conditions, stored and executed on a blockchain platform. |

| Mining | A process by which new transactions are validated and added to the blockchain, thereby creating new blocks. |

| Distributed ledger | A decentralised database that maintains a continuously growing list of records or blocks across multiple networked nodes or computers. |

How does blockchain technology work?

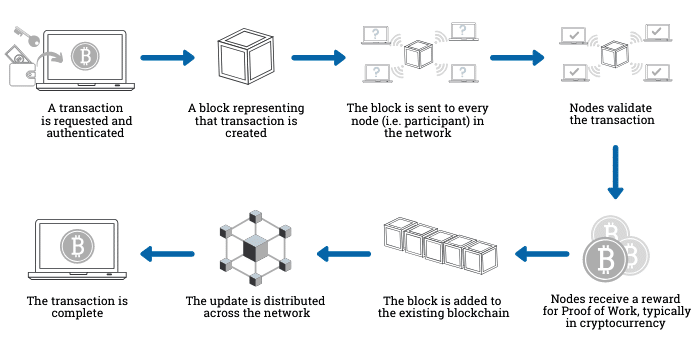

Blockchain technology organises data into blocks interconnected in chains, each containing a hash from the preceding one, a time stamp, and a digital signature of the transaction data. Before a transaction can be incorporated into the current blockchain, it undergoes several crucial steps, as illustrated in Figure 1.

Step 1: User 1 initiates the transaction to send X amount of digital cryptocurrency to User 2.

Step 2: User 1’s node begins the transaction by creating it and then digitally signing it with its private key. Transactions within a blockchain can represent various actions.

Step 3: The requested transaction is disseminated across a peer-to-peer (P2P) network and broadcast to every computer or node.

Step 4: Each node receives the request and endeavours to validate the transaction using cryptographic algorithms. The node that completes the validation process is known as the miner node, which is rewarded with cryptocurrency.

Step 5: The validated blocks are then appended to the existing blockchain network. These nodes are interconnected through the concept of hashing.

Step 6: These authorised transactions are recorded in a public ledger. Once a block is incorporated into an existing chain, transactions are finalised, and the ledger is updated.

Hash function working in a blockchain network

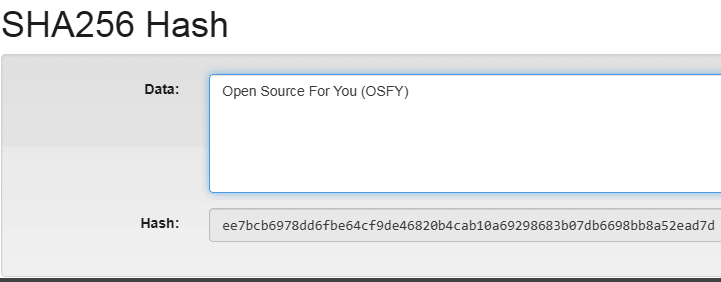

Hashing, a cryptographic technique, generates a fixed-length output when data is processed through a function. The SHA-256 hashing function is employed in the Bitcoin blockchain network. The primary objective of hash functions is to prevent the discovery of any two inputs that yield identical outputs. Two critical characteristics of a hash function are: (i) a minor alteration in a single character completely alters the hash value, and (ii) it operates as a one-way function, which means it cannot be reversed. Figure 2 demonstrates the SHA-256 hash function within the blockchain network.

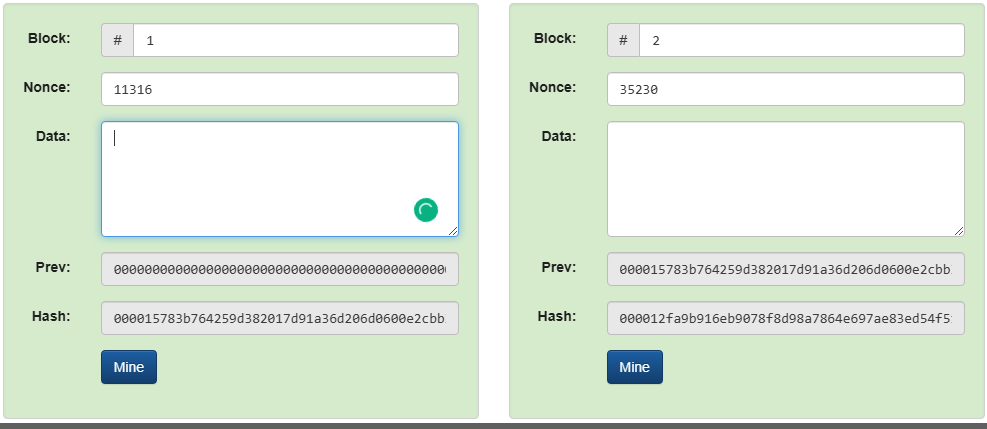

Each block node has a complete copy of the distributed ledger within a blockchain network. As illustrated in Figure 3, a valid block hash begins with four leading zeros, indicating its validity. Each new hash is generated by combining the previous hash, the new transaction block, and a nonce. The difficulty of the hash, determined by the number of leading zeros it must have, regulates the speed of block production to approximately one block every 10 minutes. A higher difficulty makes it more challenging for anyone to alter the blockchain and use it for double spending.

Comparison of popular blockchain platforms

Blockchain technology has spurred the development of various platforms, each with its unique features and capabilities. Table 2 compares popular blockchain platforms that are driving innovation across industries.

Table 2: Popular blockchain platforms

| Criteria | Ethereum | Hyperledger Fabric | R3 Corda | Quorum |

| Type | Public | Permissioned | Permissioned | Permissioned |

| Target industry | General-purpose blockchain platform | Various, but primarily enterprise | Financial services, supply chain, healthcare | Financial services, enterprise |

| Programming built-in | Solidity | Go, Java, JavaScript | Java, Kotlin | Solidity, Go, Java |

| Governance | Ethereum developers | Linux Foundation | R3 Consortium | J.P. Morgan and network participants |

| Cryptocurrency used | Ether | Can integrate with various cryptocurrencies | Not applicable (permissioned network) | Quorum ERC-20 tokens, but can incorporate other cryptocurrencies |

| Privacy feature | Limited | Supported | Supported | Supported |

| Consensus mechanism | Proof of Work (PoW) | Pluggable framework | Pluggable (supports various consensus algorithms) | Pluggable (based on Ethereum) |

| Complexity | High complexity | Moderate– requires understanding of Fabric architecture | Moderate– requires understanding of Corda flows and states | Moderate–requires understanding of Ethereum-based architecture |

| Transaction fees | Gas fees vary based on network demand | Configurable by network operators | Not applicable (permissioned network) | Configurable by network administrators |

Top 10 blockchain startups in 2024

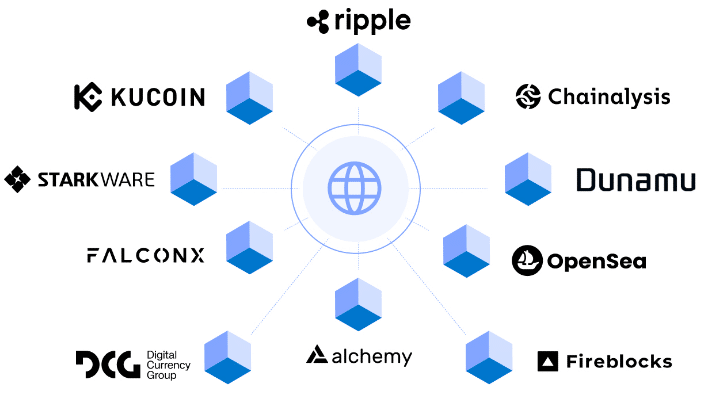

Venture capitalists, private equity firms, and alternative investment funds have shown substantial interest in blockchain and cryptocurrency companies, drawn by their groundbreaking approaches to finance and commerce. Over the past three years, these companies have collectively raised approximately $73 billion. Figure 4 lists the top crypto and blockchain startups in 2024, featuring standout names from the NFT industry, emerging blockchain developers in the Layer 2 sector, and various crypto brokerages.

Blockchain technology reshapes industries by offering secure, transparent, and efficient solutions to longstanding challenges. It is providing endless opportunities in the critical areas of healthcare, the financial sector, accounting, and the online marketplace. The popularity of blockchain technology will continue to gain momentum, offering unique career opportunities to those interested in it.