The potential for increased security, efficiency, and transparency that blockchain offers is too significant to ignore. It is evolving and disrupting traditional systems, proving that it has real industry altering powers.

Blockchain is a disruptive technology that digitises, decentralises, secures and incentivises the validation of transactions across industries. This technology has the potential to improve security, processes and systems in every domain where accurate, tamper-proof record-keeping is essential.

Trust: Blockchain is a decentralised, peer-to-peer network that records transactions to blocks, which are written to the distributed ledger based on consensus between all the participants in the network. The ledger is distributed to all the nodes and is not centralised. These factors foster trust among the participants.

Transparency: The data recorded on the blockchain ensures all the participants in the network have the distributed ledger copy; no party can maliciously change the data in the ledger, as the transaction is committed to the blockchain once all parties come to a consensus (based on applicable consensus algorithm).

Elimination of intermediaries: Blockchain technology eliminates the need for intermediaries. Once blockchain technology is adopted, consensus algorithms transparently record and verify transactions, eliminating the need for manual verifications by any third party. Cryptography helps in eliminating third-party intermediaries as keepers of trust.

Automation: With transactions executing almost immediately and significantly reducing the processing times (sometimes from days to hours), old time-consuming processes are replaced by automated verification and validation.

Key characteristics of blockchain technology

Digital: Digitises all the information on the blockchain, thus eliminating the need for manual documentation.

Distributed: Blockchain distributes control among all peers in the transaction chain, creating a shared infrastructure within an enterprise system. Participants independently validate information without centralised authority. There is no single point of failure because of distributed system operation. Even if one node fails, the remaining nodes continue to operate, ensuring no disruption.

Immutable: All the transactions are immutable in the blockchain. Encryption is done for every transaction covering time, date, participants, and hash to the previous block.

Chronology: Each block acts like a repository that stores information pertaining to a transaction, and links to the previous block in the same transaction. These connected blocks form a chronological chain providing a trail of the underlying transaction.

Consensus based: A transaction on the blockchain is executed only if all the parties on the network unanimously approve it. Consensus-based rules can be altered to suit various circumstances.

Digital signature: Blockchain enables exchange of transactional values using unique digital signatures that rely on public keys. Public keys are decryption code known to everyone on the network. Private keys are codes known only to the owner to create proof of ownership. This is very critical to avoid fraud in records management.

Consistent: Blockchain data is complete, consistent, timely, accurate, and widely available.

Persistence: No invalid transactions are admitted. It is nearly impossible to delete or roll back transactions once they are included in the blockchain. Cryptographically, the blocks created are sealed in the chain. It is impossible to delete, edit or copy already created blocks and put them on the network. This ensures a high level of robustness and trust.

Anonymity: Each user can interact with the blockchain with a generated address, which does not reveal the real identity of the user.

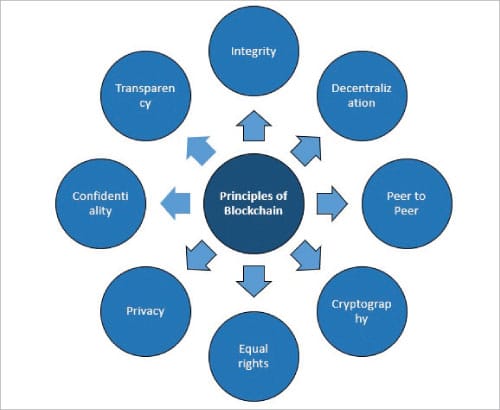

Principles of blockchain

Integrity: Blockchain technology uses a distributed verification system for transactions that does not centralise power. Integrity is required during the decision rights of blockchain users and a network’s incentive structures. The use of complex algorithms and consensus among users ensures that once agreed upon, there is no tampering with transaction data. Data stored on blockchain acts as a single version of truth for all parties involved, reducing the risk of fraud.

Decentralisation: Blockchain distributes power among different members. This means no single person or system can ever tamper with it. It is robust and resistant to attacks and fraud due to a distributed power system.

Peer-to-peer: All blockchain transactions are peer-to-peer. This means that at least two parties are involved. The best way to understand this is to compare a standard credit card transaction with the first practical use of blockchain. The benefits of the peer-to-peer aspects of the blockchain are that the two people involved in a transaction can both verify if the transaction is correct, without the need for any other party to be involved.

Cryptographic system: Blockchain lends its cryptography a level of authenticity and integrity.

Equal rights: Rights are reserved in a transparent manner. Blockchain users know exactly what rights they are entitled to and that they are equal and fair in the best way possible.

Privacy: Blockchain establishes a separate virtual identity for its users to protect their privacy, both online and offline. The identity uses a series of numbers, much like code, that are difficult to profile. Hence, blockchain fosters trust by eliminating the need for any real (or seemingly real) identity. It protects the identity of its users so that they can participate in the digital economy freely and fairly with integrity.

Confidentiality: Blockchain provides confidentiality by enabling users of a ledger to see authorised transactions only.

Transparency: Blockchain shares the ledger to all nodes and uses consensus algorithms to reach consensus among them. Consensus algorithms also ensure the ordering and execution of the transactions.

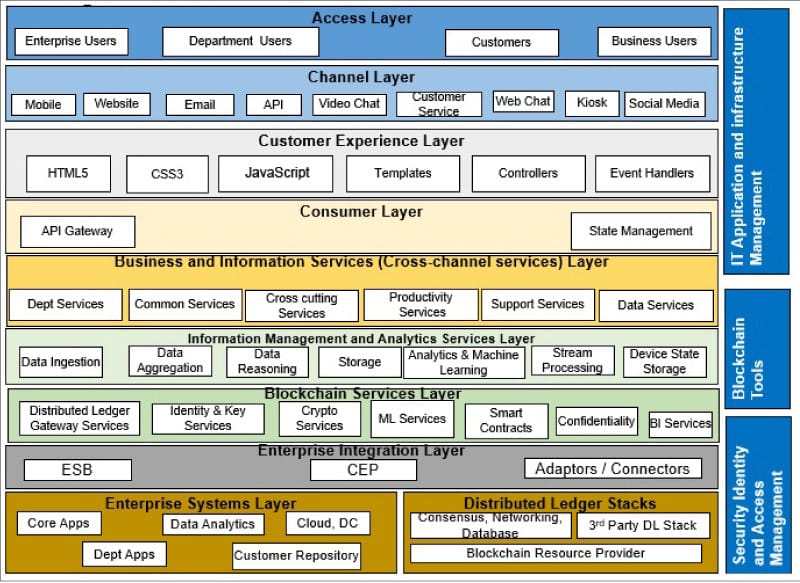

Figure 2 shows the logical application architecture of the blockchain system with key components and layers.

Blockchain services layer acts as a gateway for reaching out to the blockchain infrastructure. It consists of various services related to identity management, key management, cryptography, machine learning (ML) and business intelligence (BI). Identity, key, and cryptographic services are critical for data integrity. BI and ML are used for analysis and reporting purposes.

Distributed ledger stack consists of the core distributed ledger technology stack. Blockchain building, transaction execution and consensus happen in this layer. The components in this stack may vary depending on the distributed ledger product chosen. However, the common sub-components are consensus algorithms, data storage, and transactions management and other relevant services.

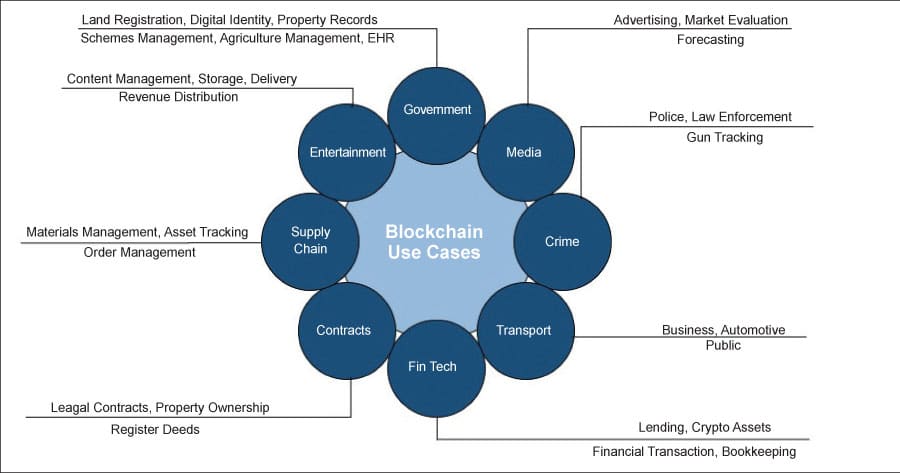

Real world use cases of blockchain technology

Government

In government, linking the data between various departments with blockchain ensures that the data is realised in real-time. Blockchain technology could improve transparency and check corruption in governments worldwide.

- Registration: By securing a unique and non-corruptible record on a blockchain and validating changes to the status of that record across owners, a reliable property record can be created, whether for a piece of land that heretofore had no owner or as a link between stovepiped systems. A decentralised, standardised system for land registration records could reduce the number of intermediaries required, increase trust in the identity of transacting parties, increase process efficiencies, and decrease time and cost to process.

- Election: Citizens can cast votes the same way they initiate other secure transactions and validate that their votes were cast—or even verify the election results. Solutions are being worked on to blend secure digital identity management, anonymous vote-casting, individualised ballot processes, and ballot casting confirmation verifiable by the voter. Potential cost savings can be achieved through blockchain-enabled voting.

- Finance: Online identity has always been a time-consuming and costly process. Financial services like loans, mortgages, and insurance have always required a higher level of security, checking, authentication and authorisation. This meant that checking official government identity documents was a required step. One of the benefits of the blockchain is that it has the potential to cut out the intermediaries and provide every organisation/department in the network access to the same source of the right information. Blockchain technologies make tracking and managing digital identities secure and efficient, resulting in reduced fraud. Users are able to choose how they identify themselves and with whom their identity is shared.

- Town planning: Having property records on the blockchain makes it possible that prospective buyers shall verify the owner of a house quickly and easily.

- Revenue: Blockchain enables seamless cross-referencing of documentation across multiple government entities. All documentation is automatically verified by the relevant entities. The inherent features of blockchain (digital identity) make it impossible to make changes to the ledger.

- Managing entity: Business unit incorporation and governance is possible with the use of digital signatures and programmable business rules. It also enables approvals and validations of the entity and its application on the blockchain. The distributed ledger technology (DLT) allows multiple parties to digitally sign for authorisation and approve a transaction and documents.

- Grants: An integrated blockchain solution enables seamless customer onboarding with automated disbursements of loans and grants. Transactions on the ledger are auditable in real-time providing greater transparency for regulators. Highly secured digital signatures make sure transactions get executed only when the relevant entities provide their signature.

- Agriculture: Integrated agriculture management system (IAMS) with a blockchain infrastructure ensures immutability of data and a way to trace historical agricultural data, as agricultural products move from production sources to the consumer. IAMS with a blockchain infrastructure helps diversify current agricultural management practices in a way that engages the public through ownership of the agricultural production process. Other possible applications include the use of blockchain technology to record and manage agricultural land records as well as agriculture insurance.

- Healthcare: Digitisation of health records is a significant task in the public health sector, which is huge, complex and associated with ethical issues. Medical records are scattered and erroneous, with inconsistent data handling processes. Sometimes, hospitals and clinics are forced to work with incorrect or incomplete patient records. Blockchain technology can help create a secure and flexible ecosystem for exchanging a patient’s electronic health records. This technology can also make the space more transparent by creating a basis for critical drugs, blood, organs, etc. In addition, by putting all medical licences on a blockchain, fraudulent medical practitioners can be prevented from practising, and chemists can be prevented from selling spurious drugs.

- Education: Student records, faculty records, educational certificates, etc, are key assets in the education domain and are shared with multiple stakeholders; so it is imperative to ensure that they are trustworthy. All these records can be maintained with the application of blockchain technology. Blockchain can also simplify certificate attestation and verification.

Media

Media is a multi-billion dollar industry that is evolving every year. However, it is currently not consumer- or creator-friendly due to intermediaries taking advantage and making tons of revenue in the process. With blockchain, the whole landscape can change and become more accessible to consumers as well as content creators.

Advertising: Advertisers can use blockchain to place their ads and earn revenue in millions of dollars. With blockchain-powered browsers, it is now possible for consumers to turn off the advertising and protect their privacy at the same time.

Market evaluation/forecasting: Blockchain can speed up market forecasting to an entirely new level, as it can hold a massive amount of data that can be used in conjunction with machine learning or artificial intelligence.

Crime management

Blockchain can help enforce the law and ensure that crime remains at an all-time low.

- Police/law: The blockchain maintains integrity of data and helps in storing all the evidence. In addition, it is distributed without worrying about tampering. It adds the necessary layer of security that adds trust to law enforcement.

- Gun tracking: With blockchain, we can have a system where each gun can be accounted for. Each weapon that leaves the factory can be tracked to help stop illegal gun usage and export. Once stored, the information can be retraced whenever needed. A gun used in a crime can be traced back to its original owner or its origins can be known instantly.

Transportation

The transportation industry can be transformed by blockchain adoption. It lowers processing and administrative costs, minimises disputes, improves overall transportation speed, and much more.

- Business transportation: Blockchain allows easy data coordination using DLT. Smart contracts can be used to automate most of the transportation pipeline, or to create a custom solution to enable transportation for fragile and sensitive products easily. The whole network can scale to include more transportation vehicles, products, and information.

- Automotive: With self-driving cars already out and shipping, it is now high time for the automotive industry to make use of the blockchain. The revolution has already started. The IOTA (Internet of Things Application) blockchain has already shown a proof-of-concept for how its Tangle DLT can work for autonomous cars.

- Public transport: Public transportation always demands improvement. With blockchain, things can change drastically.

Fintech

Right now, tons of fintech start-ups are working to provide a better solution by using blockchain.

Blockchain is the greatest disrupter to the global financial services system of this generation. Banking systems and principles, underlying banking transactions, and bookkeeping are complex and challenging. With a blockchain-based solution in place, complex processes that once took weeks to reconcile can be completed in a few minutes.

Existing ledger accounting in the financial services sector is usually in the form of a centralised and private database, not too different from the paper based versions used a long time back. With blockchain, the ledger moves to an open and distributed record shared across the participant nodes in the blockchain. Each node maintains its own version of the ledger, and the network must collectively agree on the authenticity and correctness of transactions before carrying out an update.

Contracts

Contracts help to set up requirements for taking up a job, for payment and any other tasks that require two parties. They can be related to music, land, property, etc.

- Inheritances: Smart contacts empower digital inheritance, which means to transfer digital assets to someone.

- Legal contracts: Legal contracts can take advantage of smart contracts. However, they must adhere to the blockchain law.

- Property and land: Blockchain can provide a suitable means to register deeds, property ownership, and so on. This will remove any frauds, and any change of deed is brought to the notice of the owner. In addition, the information can be backtracked with full transparency and security.

Supply chain management

In supply chain, blockchain technology can be used to store and record all the transactions and exchanges of ownership, right from the extraction of raw materials to delivery to the customer. It helps to identify where the materials were sourced, the type of labour used, and the exact position of the goods at any given moment.

In supply chain management, blockchain technology enables enterprises to:

- Verify materials

- Identify asset quantity as the assets move through the supply chain

- Coordinate orders and shipment notifications

- Verify the constitution of materials

- Increase scalability, security, and innovation

- Link physical materials to serial numbers, bar codes, and digital tags

- Share important information about the manufacturing process, assembly, delivery, and vendors

Entertainment

Blockchain is also changing the entertainment industry in several ways.

- Entertainment industry: The future of entertainment is in the hands of the blockchain. Blockchain will change how content is created and consumed.

- Music industry: Blockchain will make it easier to share music and use smart contracts to do so. The smart contracts will ensure that the revenue is distributed to the parties according to the agreement. It will also remove intermediaries.

Benefits of blockchain

- Greater transparency; transaction histories are becoming more transparent using blockchain technology

- Enhanced security; there are several ways that blockchain is more secure than other record-keeping systems

- Elimination of error handling through real-time tracking of transactions with no double spending

- Improved traceability

- Trusted record-keeping and shared trusted process

- Increased efficiency and speed, reduction of settlement time to mere seconds by removing intermediaries

- Reduced cost and complexity, material cost reduction through the elimination of expensive proprietary infrastructure

- Full automation of transactional processes, from payment through settlement

Blockchain is not recommended for:

- High performance (millisecond) transactions

- Small organisations (no business network)

- Database replacement

- Messaging solutions

- Transaction processing replacement

Table 1 shows various open source blockchain products and their critical characteristics.

| Feature | Open source product | Remarks |

| Public blockchain | Ethereum, Ripple, Litecoin, etc | Permissionless blockchain; participants are anonymous and proof of work as consensus algorithm; requires mining |

| Private blockchain | Hyperledger projects, Exonum, OpenChain, MultiChain | Permissioned blockchain; identity of the participants is known before; no need of mining and native cryptocurrency to pay for mining |

| Federated blockchain (consortium) | R3, EWF, etc | Group of companies or individuals coming together to make decisions for the best benefit of the whole network. Such groups are also called consortiums or a federated blockchain |

| Smart contracts in general programming languages | Hyperledger, Ethereum | Ethereum does not directly support Java; it does so with the help of a framework called web3j |

| No mining and native cryptocurrency | Hyperledger, Corda, Openchain | Typically, public blockchains require mining (as part of proof of work) to add a block to the chain. Miners will be rewarded using native cryptocurrency |

| Pluggable consensus algorithms | Hyperledger, Corda, OpenChain | Support for pluggable consensus used for different applications |

| Pluggable ordering service | Hyperledger | Support for pluggable ordering service used for different applications |

| Pluggable membership service | Hyperledger | Support for pluggable membership used for onboarding new users onto the network |

In summary, blockchain provides better security during transactions of any value. This unique and universal technology helps to streamline and automate nearly all customer services and legal contracts, while increasing the transparency and effectiveness of an enterprise. However, more work is needed for using blockchain technology to minimise enterprise costs, improve security in an era of cyber uncertainty and enhance customer delivery.

Disclaimer: The views expressed in this article are that of the author and HCL does not subscribe to the substance, veracity, or truthfulness of the said opinion.